Jan 5, 2015

Inflation as Chronic Illness

When COVID-19 emerged in early 2020, policymakers across the world scrambled to respond. Their instincts failed them—and us. They locked economies, confined healthy people with sick ones, and closed schools, leaving children with learning deficits from which they might never recover. Every government threw gobs of money out windows as if this largesse were costless. It was as shortsighted and destructive as government responses usually are.

While governments around the globe spent exorbitant sums of money on the pandemic problem, few were as irresponsible as our representatives in the United States. Within the span of a year, Congress, two successive administrations, and the Federal Reserve responded with an unprecedented fiscal and monetary expansion, injecting trillions of dollars into the economy to pay for, among other things, the mass unemployment and business failures they themselves had created. While these interventions were framed as necessary emergency measures, they created long-term distortions that fueled inflation, undermined economic recovery, and exacerbated labor shortages.

The result was the highest US inflation in 40 years, a labor market riddled with perverse incentives, and government dependency that outlasted the crisis. The inflation surge was not an inevitable consequence of the pandemic but rather the predictable outcome of excessive demand fueled by unchecked government spending. This article examines the fiscal and monetary missteps of the COVID-19 response—the timewave of programs often duplicating and contradicting each other including the Paycheck Protection Program (PPP), enhanced unemployment benefits, and corporate bailouts—and the inflation that resulted from the recklessness.

A Despotic Moment

Before considering the economic implications, I should first note that the most striking aspect of the pandemic response was the unprecedented level of government intervention in economic life. Under emergency public-health mandates, authorities dictated which businesses could remain open and which must be shuttered, imposed sweeping travel and commercial restrictions, and expanded regulatory control to a degree unseen in modern American history.

At the height of the pandemic, 43 state governors imposed stay at home orders, effectively shutting down businesses they deemed “non-essential.” As a result, millions of workers were forcibly idled—a scenario unimaginable before 2020. Empirical evidence to justify these policies on public-health grounds was weak. As economist David Henderson points out, decisions were often driven by worst-case projections rather than by solid data. The economic fallout was catastrophic: by April 2020, unemployment had surged to nearly 15 percent, and GDP contracted by approximately 20 percent during 2020. Studies indicate that more than half of job losses and economic contractions were due to government-imposed restrictions, not the virus itself.

Equally alarming was the arbitrary nature of essential vs. non-essential designations. Large corporate retailers, certain manufacturers, and liquor stores remained open, while small businesses, restaurants, gyms, and independent retailers were forced to close. Many entrepreneurs saw their livelihoods destroyed overnight. The notion that bureaucrats could decide whose job and business mattered and whose did not was a profound and counterproductive violation of economic liberty.

Even after the worst of the crisis had passed, government overreach continued. Among the most egregious examples is the federal eviction moratorium imposed by the CDC, which effectively nullified private rental contracts nationwide for over a year. The US Supreme Court eventually struck down this moratorium as unconstitutional, but the fact that such an order was issued in the first place set a dangerous precedent. Temporary emergency measures have a way of becoming permanent expansions of state power.

Free Money for Everyone

Executive overreach was terrible, but legislative action was also massive and incoherent. Legislators rushed to pass as many relief programs as possible, with little regard for redundancy or contradictions. This led to overlapping, and at times conflicting, benefits. For example, the Paycheck Protection Program (PPP) and enhanced unemployment benefits—covered below—worked against each other. One aimed to keep employees on payroll, while the other provided generous jobless benefits that often exceeded prior wages, discouraging work.

Additionally, politicians sent direct individual checks to nearly everyone, on top of expanded unemployment benefits, paid leave benefits, and business subsidies. As a result, many individuals ended up with more disposable income than they had before the pandemic. Yet, the administration still paused student loan payments and set the rates at 0 percent between March 2020 and September 2023, even for borrowers who were still employed. This scattershot approach created a system where aid distribution was not based on actual need, leading to economic distortions and inefficiencies.

As an example, consider the expansion of unemployment benefits, particularly the $600-per-week federal supplement. This created severe labor-market distortions by making it more lucrative for millions of workers to stay unemployed rather than return to work. At its peak, two-thirds of unemployed workers were receiving more in benefits than they earned while working, with some earning up to 145 percent of their previous wages by staying home. These handouts reduced the incentive to work even as businesses struggled to fill job openings. Employers across sectors—particularly in hospitality, retail, and manufacturing—reported extreme difficulty in rehiring workers. The Federal Reserve’s Beige Book surveys repeatedly highlighted how labor shortages were at least partially driven by these distorted incentives.

While supporters of the enhanced UI argued that it was necessary for economic stability, reality proved otherwise. States that ended these benefits early saw faster employment recoveries, while states that maintained them faced persistently high rates of unemployment. By mid-2021, as demand surged, businesses were forced to offer inflated wages and hiring bonuses to lure workers back—costs that were passed on to consumers, further exacerbating inflation.

Adding insult to injury, the amount of fraud in the program was enormous. According to the Government Accountability Office, “the amount of fraud in unemployment insurance (UI) programs during the COVID-19 pandemic was likely between $100 billion and $135 billion.”

What’s truly infuriating about this entire episode is the sheer arrogance of economists and policy scholars who dismissed concerns about inflation as if it were a relic of the past.

As this dynamic was being played out across the states, the Payroll Protection Program, a $953 billion flagship pandemic program, aimed to provide forgivable loans to small businesses to retain employees. While this program was intended to prevent layoffs, it became a prime example of wasteful government spending, fraud, and misallocation of resources. For one thing, loans were distributed with minimal vetting, leading to widespread fraud estimated at over $100 billion. Large, well-capitalized corporations, including publicly traded companies and law firms, received massive payouts, while many truly struggling small businesses were left behind.

Moreover, PPP funds disproportionately went to industries and regions that were not among those hardest hit by the pandemic. Indeed, a significant portion of the money flowed to businesses that were never at risk of failing or employees not at risk of losing their jobs. It means that a majority of the money had little to no economic impact.

The unintended consequences of PPP were also severe. By artificially propping up payrolls, the program delayed necessary economic adjustments and prevented labor reallocation to more productive sectors. Rather than allowing businesses to adapt to new market conditions, the government subsidized inefficiency and kept unviable firms afloat. A more market-oriented approach would have relied on liquidity loans rather than broad-based, taxpayer-funded handouts.

And, of course, no emergency response would be complete without massive transfer to the states, ostensibly justified by fear that their revenue would dry out—it didn’t—and also loads of cronyism. I don’t have enough words to cover how both went terribly wrong. However, I will note that one of the most egregious examples of government overreach during the pandemic was the bailout of the airline industry. Airlines received $54 billion in taxpayer-funded aid, supposedly to prevent mass layoffs. Yet as soon as the subsidy period expired, airlines laid off thousands of workers anyway. These bailouts did not save jobs in the long run, but they did protect airline shareholders and executives from financial losses.

This bailout culture sets a dangerous precedent. Rather than building cash reserves for downturns, and instead of encouraging cash-strapped companies to restructure through Chapter 11 bankruptcy, the government intervened, reinforcing the expectation that taxpayers will rescue mismanaged firms in future crises. As the head of Delta, Ed Bastian, told his shareholders, the main pandemic lesson was that the government had the airlines’ backs—meaning that the government will compel taxpayers to relieve airlines and other politically influential industries of the need to prudently prepare for, and to deal with, hard times.

A better approach would have let airlines and other large corporations adapt or fail on their own terms, rather than artificially propping them up with public money. Government intervention only postpones the inevitable, while adding to the national debt.

A Foreseeable Problem

No commentary on the COVID-19 policy response can ignore the consequence of this fiscal delinquency as evidenced by the surge in inflation, which peaked at 9.1 percent in mid-2022—the highest level since 1981. Cumulative over 4 years, the Biden admin oversaw 22 percent inflation. Inflation does not rise in a vacuum; it is the result of too much money chasing too few goods. The primary driver of this inflation was the federal government’s decision to unleash an unprecedented wave of deficit-financed spending, far exceeding the actual economic contraction caused by the pandemic.

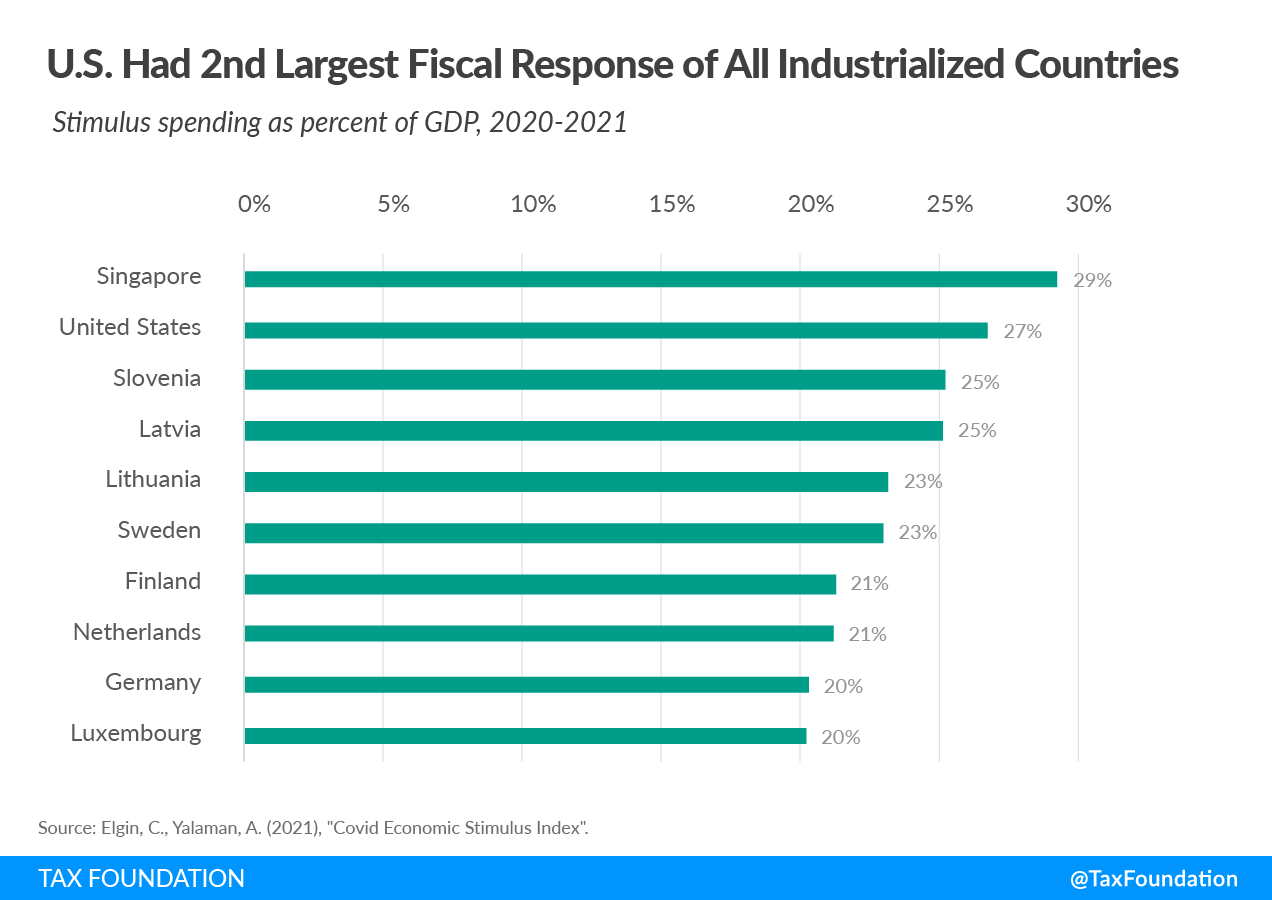

From March 2020 to early 2021, the US government injected close to $6 trillion into households and businesses in the form of stimulus checks, enhanced unemployment benefits, and business aid programs. That’s 27 percent of GDP. This flood of money occurred while the economy’s supply side was restricted by lockdowns, supply-chain disruptions, and labor shortages.

Even by Keynesian standards, the fiscal response was excessive. The estimated output gap—the difference between potential GDP and actual GDP—was around $2.3 trillion, yet the size of the government stimulus was nearly three times that amount. The same is true of the $1.9 trillion American Rescue Plan (ARP), which was passed in March 2021. At that time, the economy was already rebounding, and the remaining output gap was only about $700 billion over the next two years during which the money was to be spent. Despite this reality, the Biden administration proceeded with another wave of unnecessary spending.

I think this point is worth repeating. Inflation is a large part the result of Biden’s disregard of the old fiscal religion that holds that, while the government may deficit-spend during recessions, the aftermath requires austerity. By trying to pass the $3 trillion Build Back Better bill—legislation that attempted to make permanent many of the temporary Covid programs—closely following the ARP and an infrastructure bill, and then passing the Inflation Reduction Act (IRA) and the Chips Act, the government sent strong signals to investors that borrowing might never again be matched with primary surpluses to retire the debt. The resulting inflation was inevitable.

The Federal Reserve played a critical role in facilitating this inflationary spiral by keeping interest rates near zero and purchasing massive amounts of government debt ($2.7 trillion), flooding markets with excess liquidity. The Fed total intervention was around $4.7 trillion. While Fed officials initially promised that the resulting inflation was “transitory,” it became clear by mid-2021 that economy-wide price increases were persistent. By the time the Fed began tightening monetary policy, inflation had already taken root, forcing aggressive rate hikes that have now led to financial instability and increased recession risks.

What’s truly infuriating about this entire episode is the sheer arrogance of economists and policy scholars who dismissed concerns about inflation as if it were a relic of the past. They genuinely believed that inflation had been permanently conquered and that, in the unlikely event it did return, the Fed had the tools to handle it—so why worry? The casual indifference with which they brushed aside these warnings is astonishing, especially considering that the Fed’s primary “tool” for fighting inflation is to deliberately slow down the economy—a process that inevitably hurts millions of people, particularly the most vulnerable. That so many economists were so cool and detached about this trade-off is nothing short of maddening.

If this crisis has taught us anything, it’s that we should demand that the Fed prioritize price stability over anything else since its ability to “take care” of inflation is far weaker than many economists smugly assumed. Nearly three years into the Fed’s tightening cycle, inflation is not only still around—it’s picking back up. Yet the same people who so confidently dismissed concerns about inflation face no consequences for their errors, while ordinary Americans continue to pay the price.

We will be debating the COVID response for years. However, a few things are indisputable. People may have liked all the money they got during the pandemic, but a lot was lost, too. The Economic Freedom of the World (EFW) Index published by the Fraser Institute measures economic freedom based on government size, legal system strength, sound money, trade openness, and regulatory burden. Before COVID-19, the US ranked among the top economically free nations, but the pandemic triggered a sharp decline. By 2020, the US fell to 7th place globally, marking its lowest ranking since 1975. The index data showed a significant drop in the US score, erasing years of progress in economic freedom. This decline was primarily driven by the federal government’s unprecedented spending surge, loose monetary policy, business lockdowns, and trade restrictions, all of which expanded the government’s role in the economy while curtailing individual choice.

While the pandemic’s impact on economic freedom was global, the US’s setbacks were particularly stark. Unfortunately, economist Robert Higgs’s “ratchet effect” describes how crises lead to permanent increases in government authority. The Great Depression, World War II, and the post-9/11 era all saw new emergency measures that permanently diminished economic and individual freedom. I fear the Covid Pandemic emergency will be no different.

{kind=link}